Risks, Rewards, and Strategies

Private money lending, also known as private lending or peer-to-peer lending in real estate, involves individuals or private companies providing loans to real estate investors. It has emerged as a powerful strategy for both investors and lenders. This alternative form of financing bypasses traditional lending institutions, offering unique opportunities and challenges. Whether you’re considering becoming a private lender or seeking private money for your real estate investments, understanding the intricacies of this practice is crucial.

Key Characteristics of Private Money Lending:

- Faster approval process

- More flexible terms

- Higher interest rates

- Shorter loan durations

- Less stringent qualification criteria

Private lenders for real estate play a crucial role in the industry, often funding deals that traditional banks won’t touch. They can be individuals with capital to invest, groups of investors pooling their resources, or companies specializing in private lending.

Types of Real Estate Deals Funded by Private Money:

- Fix-and-flip projects

- Buy-and-hold rental properties

- Land development

- Commercial real estate acquisitions

- Bridge loans for quick property purchases

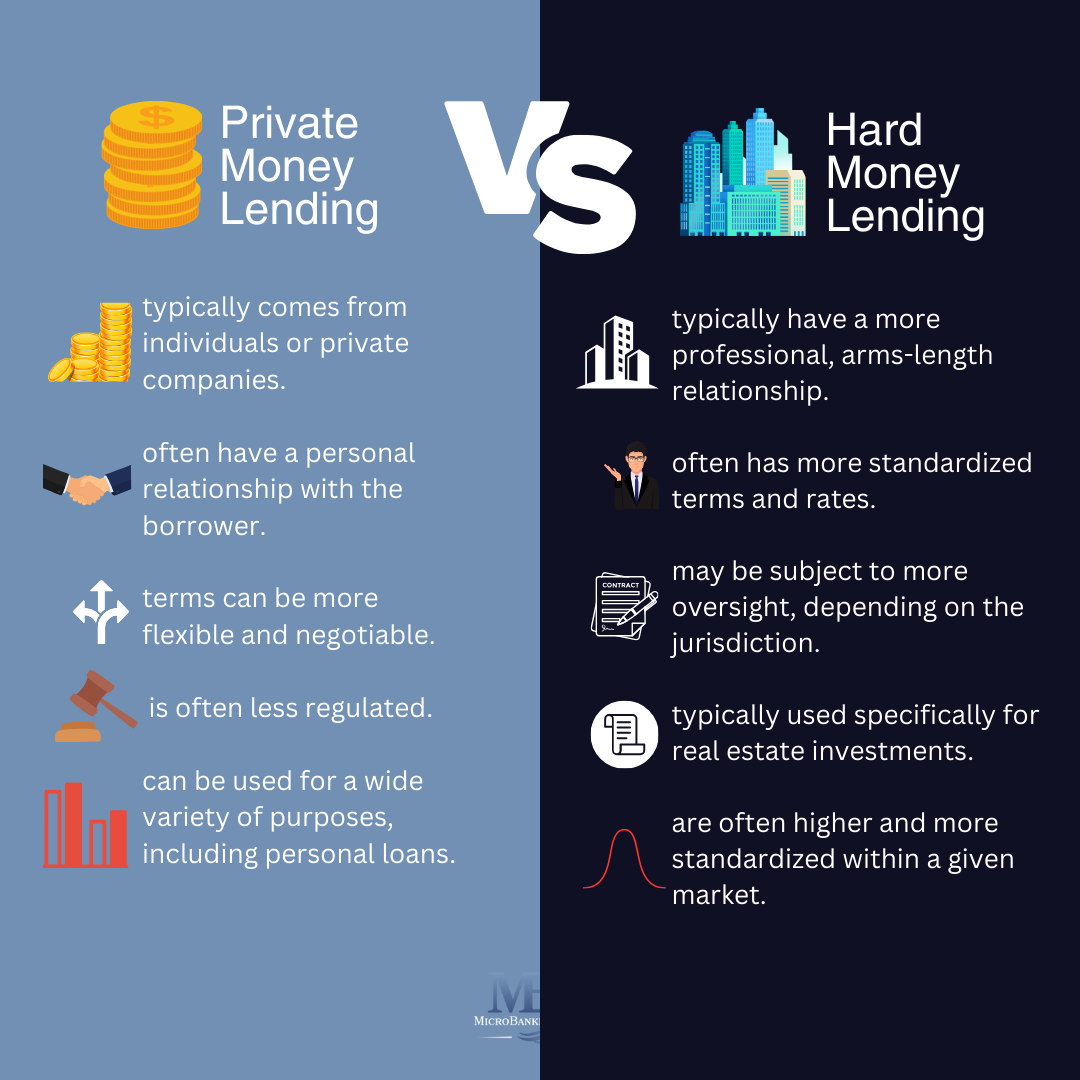

The Difference Between Private Money Lending and Hard Money Lending

While often used interchangeably, private money lending and hard money lending have some distinct differences:

- Source of Funds:

- Private money typically comes from individuals or private companies.

- Hard money usually comes from companies or groups specifically set up for lending.

- Relationship:

- Private money lenders often have a personal relationship with the borrower.

- Hard money lenders typically have a more professional, arms-length relationship.

- Terms:

- Private money terms can be more flexible and negotiable.

- Hard money lending often has more standardized terms and rates.

- Regulation:

- Private money lending is often less regulated.

- Hard money lending may be subject to more oversight, depending on the jurisdiction.

- Loan Purpose:

- Private money can be used for a wide variety of purposes, including personal loans.

- Hard money is typically used specifically for real estate investments.

- Interest Rates:

- Private money rates can vary widely based on the relationship and deal specifics.

- Hard money rates are often higher and more standardized within a given market.

Despite these differences, both private money and hard money lending serve similar purposes in the real estate market, providing alternative financing options for investors.

The Rewards of Private Money Lending

For those with capital to invest, private money lending can offer several attractive benefits:

- Higher Returns: Private money loans typically offer higher interest rates than traditional investments, often ranging from 8% to 12% or more. Example: A $100,000 private money loan at 10% interest could yield $10,000 in annual interest income.

- Passive Income: Once the loan is made, the lender can enjoy regular interest payments with minimal ongoing effort.

- Asset-Backed Security: Loans are secured by real estate, providing a tangible asset as collateral.

- Diversification: Real estate lending can diversify an investment portfolio beyond stocks and bonds.

- Control: Private lenders have more control over their investments compared to buying shares in a REIT or real estate fund.

- Flexibility: Lenders can choose which projects to fund and negotiate terms that suit their needs.

- Potential for Equity Kickers: Some private money deals include profit sharing or the option to convert debt to equity.

- Networking Opportunities: Private lending can lead to valuable connections in the real estate industry.

The Risks of Private Money Lending

While the rewards can be significant, private money lending also comes with its share of risks:

- Default Risk: There’s always a possibility that the borrower may fail to repay the loan. Mitigation Strategy: Thorough due diligence on the borrower and the property, and maintaining conservative loan-to-value ratios.

- Property Value Fluctuations: If the property value declines, the collateral may not cover the loan amount in case of default. Mitigation Strategy: Regular property value assessments and adjusting loan terms if necessary.

- Liquidity Risk: Private money loans are typically not as liquid as other investments. Mitigation Strategy: Maintain a diversified portfolio and only lend money you won’t need in the short term.

- Legal Complexities: Proper documentation and adherence to lending laws are crucial to protect the lender’s interests. Mitigation Strategy: Work with experienced real estate attorneys to draft and review all loan documents.

- Market Risk: Economic downturns can impact the real estate market and the borrower’s ability to repay. Mitigation Strategy: Stay informed about market trends and adjust lending criteria during uncertain times.

- Lack of Guarantees: Unlike bank deposits, private loans are not insured by the FDIC or other government agencies. Mitigation Strategy: Diversify your lending portfolio and never lend more than you can afford to lose.

- Operational Risks: Managing loans, collecting payments, and dealing with potential foreclosures can be time-consuming. Mitigation Strategy: Consider using a loan servicing company to handle day-to-day operations.

Strategies for Successful Private Money Lending

To maximize rewards and mitigate risks, consider these strategies:

- Due Diligence: Thoroughly vet potential borrowers and their projects. Review their track record, financial statements, and the specifics of the deal.

Checklist:

✅ Borrower’s credit history and score

✅ Past real estate experience

✅ Current financial situation

✅ Project feasibility study

✅ Property appraisal

✅ Title search and insurance

- Proper Documentation: Use professionally drafted loan agreements that clearly outline all terms and conditions.

Key Elements:- Loan amount and interest rate

- Repayment schedule

- Default clauses

- Collateral details

- Personal guarantees (if applicable)

- Conservative Loan-to-Value Ratios: Lend no more than 65-75% of the property’s value to provide a cushion in case of market downturns.

- Diversification: Don’t put all your eggs in one basket. Spread your lending across multiple borrowers and projects.

Example Portfolio:- 30% in fix-and-flip loans

- 30% in rental property mortgages

- 20% in commercial real estate loans

- 20% in land development loans

- Regular Monitoring: Stay informed about the progress of the project and the borrower’s financial health throughout the loan term.

Monitoring Activities:- Regular property inspections

- Quarterly financial updates from the borrower

- Ongoing market analysis of the property’s area

- Exit Strategy: Have a clear plan for what to do if the borrower defaults. Be prepared to foreclose and take possession of the property if necessary.

- Network Building: Develop relationships with real estate professionals, including agents, appraisers, and attorneys, who can provide valuable insights and services.

- Continuous Education: Stay informed about real estate market trends, lending laws, and best practices in private money lending.

Resources:- Real estate investing books and podcasts

- Local real estate investor association meetings

- Online forums and webinars

- Real estate and finance courses

How to Become a Private Money Lender

If you’re interested in becoming a private money lender, here are the steps to get started:

- Educate Yourself: Learn about real estate investing, lending laws, and market dynamics.

- Determine Your Lending Criteria: Decide what types of properties, borrowers, and terms you’re comfortable with.

Sample Criteria:- Loan amounts: $50,000 to $500,000

- Property types: Single-family homes, multi-family up to 4 units

- Loan-to-Value ratio: Maximum 70%

- Interest rates: 8-12% depending on risk

- Loan term: 6-24 months

- Establish Your Lending Entity: Consider setting up an LLC or other business entity for your lending activities.

- Develop Your Lending Procedures: Create a system for vetting borrowers, underwriting loans, and managing payments.

- Build Your Network: Connect with real estate investors, brokers, and other professionals who can bring you lending opportunities.

- Start Small: Begin with smaller loans to gain experience before committing larger amounts.

- Consult Professionals: Work with a real estate attorney and accountant to ensure legal compliance and optimal tax strategies.

Private Money Lending from the Borrower’s Perspective

For real estate investors, private money can be a valuable source of funding. Here’s what borrowers should know:

- Advantages for Borrowers:

- Faster approval and funding process

- Ability to finance deals that banks won’t touch

- More flexible terms and qualification criteria

- Potential for relationship-based lending

- Considerations for Borrowers:

- Higher interest rates compared to traditional loans

- Shorter loan terms, often requiring a clear exit strategy

- Potential for higher fees

- The need for a solid track record or a strong deal to attract lenders

- How to Attract Private Lenders:

- Build a strong track record in real estate investing

- Develop a professional investment proposal

- Network actively in real estate investing circles

- Offer competitive terms that balance the lender’s risk and reward

- Be transparent about the deal specifics and your experience

- Preparing a Loan Request:

- Detailed project plan and timeline

- Comprehensive financial projections

- Clear exit strategy (e.g., refinance, sale, etc.)

- Personal financial statement and credit report

- Portfolio of past successful projects

Case Studies: Successful Private Money Lending Scenarios

- Fix-and-Flip Loan:

- Loan Amount: $150,000

- Property Purchase Price: $200,000

- Renovation Budget: $50,000

- Loan Term: 6 months

- Interest Rate: 12%

- Outcome: Property sold for $300,000, lender earned $9,000 in interest

- Rental Property Acquisition:

- Loan Amount: $250,000

- Property Value: $350,000

- Loan Term: 24 months

- Interest Rate: 9%

- Outcome: Borrower refinanced with a traditional bank after 18 months, lender earned $33,750 in interest

The Future of Private Money Lending in Real Estate

Private money lending is likely to continue playing a significant role in real estate investing. Several trends are shaping its future:

- Technology Integration: Online platforms are making it easier for lenders and borrowers to connect and manage loans. Example: Peer-to-peer lending platforms specifically for real estate deals.

- Increased Regulation: As the practice grows, it may face more regulatory scrutiny and oversight. Potential Changes: Stricter licensing requirements, standardized disclosure forms, caps on interest rates.

- Professionalization: More individuals and companies are specializing in private lending as a full-time business.

- Market Cycles: Economic fluctuations will continue to influence the demand for and terms of private money loans.

- Alternative Structures: New lending models, such as crowdfunding and peer-to-peer platforms, are emerging alongside traditional private lending.

- Data-Driven Decision Making: Advanced analytics and AI may play a larger role in assessing borrower risk and property values.

- Sustainable and Impact Investing: Growing interest in funding eco-friendly developments or affordable housing projects.

Conclusion

Private money lending in real estate offers significant opportunities for both lenders and borrowers. For lenders, it provides the potential for high returns and a tangible investment in real estate. For borrowers, it offers access to capital that might not be available through traditional channels.

However, like any investment strategy, it comes with risks that must be carefully managed. Success in private money lending requires diligence, education, and a clear understanding of the real estate market.

Whether you’re considering becoming a private lender or seeking private funding for your real estate investments, take the time to thoroughly understand the process, risks, and best practices. With the right approach, private money lending can be a valuable tool in your real estate investing toolbox.

Are you interested in exploring private money lending for your real estate ventures? What aspects of private lending intrigue or concern you the most? Share your thoughts and questions in the comments below!